Is 700 A Good Credit Score? What It Can Do For You

Victoria Araj7-Minute Read

UPDATED: July 10, 2024

With a 700 credit score, you fall into the “good” credit score range on the FICO® credit-scoring model. Having a credit score of 700 or above can open up a lot of financial opportunities. So, what’s the secret to getting and maintaining this number?

Let’s break down how to get a 700 credit score, how it can help you and the factors that determine your score.

Apply For A Personal Loan.

What Is A 700 Credit Score?

A 700 credit score is considered a good score. Credit scores range from 300 to 850, with 300 being the lowest and 850 being a perfect score. A 700 credit score is on the higher end of the spectrum and indicates that the potential borrower has good credit and is creditworthy.

A good credit score usually helps you qualify for a better interest rate when you apply for a loan. While interest rates vary by lender, most lenders offer the best rates to those with better credit. Lenders see borrowers with a higher credit score as lower risk and thus more likely to repay their debt.

Financial experts say those with a 760 score and above receive the best rates. If you’re starting to build credit or your credit profile is shaky, 700 is a good target. However, it still leaves room for more improvement in the future.

Time often plays a role in a good credit score. Length of credit history, history of on-time payments and time spent waiting for inquiries to roll off the credit report all factor in, for example. A 700 score is a great starting point and can be the gateway to a higher score if you put in the work to improve your credit.

What Can You Get With A 700 Credit Score?

A 700 credit score typically means you won’t be turned down for important milestones like getting a mortgage or a job. You’re also likely to be fine when a landlord checks your credit to assess whether they should rent an apartment to you.

A 700 score likewise tends to come with the perks we’ll describe next.

Ideal Financing Options

A good credit score opens up various financing options. These include the opportunity to utilize personal loans, home loans, auto loans, and the best credit card offers.

Healthy credit is important since most mortgages have a minimum credit score requirement.

Consider:

- A conventional loan typically requires a credit score of at least 620.

- An FHA loan through Rocket MortgageⓇ requires a minimum credit score of 580.

- A personal loan from Rocket LoansSM requires a minimum credit score of 640.

A borrower with a 700 credit score will likely qualify for any financing option listed above.

Lower Interest Rates

A good credit score can also save you thousands of dollars in interest payments. The Federal Funds Rate is a benchmark rate set by the Federal Reserve. This rate dictates the price at which banks can borrow money from the government. Borrowers with a credit score of 700 or higher tend to be offered rates closer to Federal Reserve rates.

Therefore, typically, the higher your credit score, the less you pay on debt expenditures. This can account for thousands of dollars in savings over the loan term.

Those with a lower credit score usually receive rates further above the federal funds rate.

More Buying Power

Good credit and a lower interest rate can increase buying power on a big-ticket item like a mortgage. You can put the money you save on interest payments toward more house (or car, or whatever you desire).

Let’s use mortgages as our example since the interest rate on a mortgage affects the monthly payment. According to ConsumerAffairs, a .25% change in interest affects your home buying power.

Perhaps you have $1,620 each month to spend on a housing payment. With a $50,000 down payment and 8.25% interest rate, you could afford around $266,000 worth of house.

By shaving .25% off your interest rate, bringing it to 8%, you could buy a home that costs closer to $271,000 with $50,000 down and still keep your monthly payment at $1,620.

This savings and increased buying power transfers over to anything you finance. From student loans to car loans, a 700 credit score can help you reap the benefits of lower interest rates.

How Much Can You Borrow With A 700 Credit Score?

An improved credit score doesn’t necessarily increase the loan amount you can borrow.

The biggest indicators of how much you can borrow are DTI and the down payment amount. The larger your down payment, the more you can borrow. Additionally, the lower your DTI or housing payment-to-income ratio, the more you can borrow.

What Makes Up A Credit Score?

Before we explore how to get a credit score of 700 or higher, you should understand the factors that make up your score. The “big three” credit bureaus – Experian™, TransUnion® and Equifax® – determine your credit score. The building blocks of any credit score are pretty much the same.

Let’s take a look at what goes into your personal credit rating.

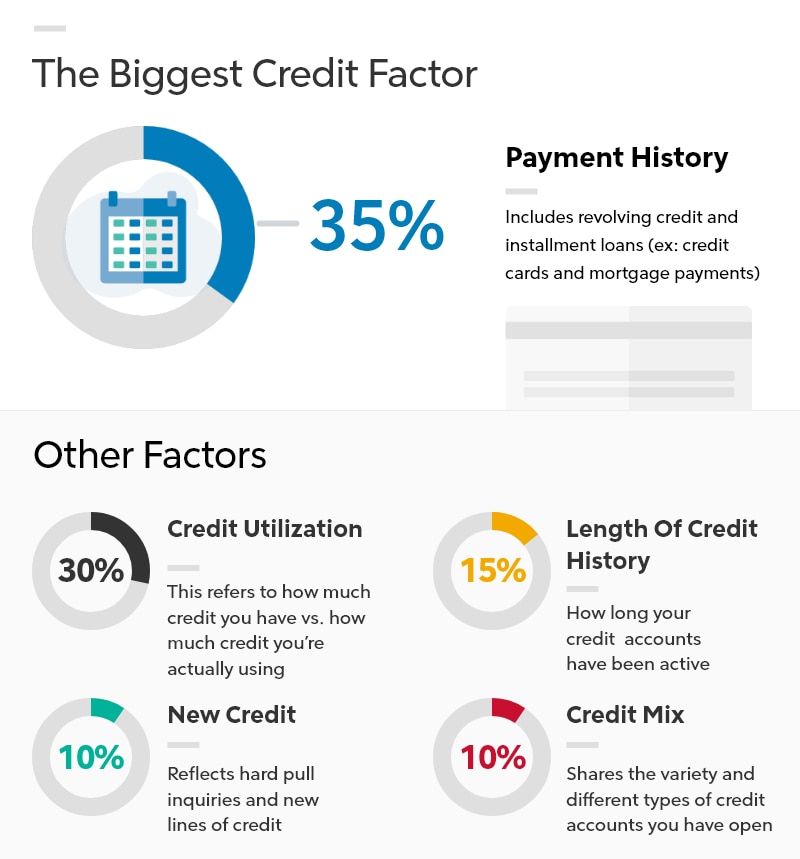

Payment History (35%)

The largest portion of a credit score is payment history. It reflects how often you make on-time payments toward your debts. Lenders want to know if you have a habit of making loan and credit card payments when or before they’re due.

Credit Utilization (30%)

Credit utilization is how much of your available credit you’re using at any given time. Lenders consider it to determine if you have a healthy relationship with credit. That is, do you carry balances each month or pay your obligations back in full?

For example, if your total credit limit is $20,000 and you borrow $15,000, your credit utilization is 75%.

The general financial best practice is to keep your credit utilization ratio at 30% or below. According to CNBC, you should keep utilization at 10% or below for an excellent credit score (800 and above).

Length Of Credit History (15%)

The longer you use credit (and keep lines of credit open), the higher your credit score will likely be. A long credit history in good standing shows lenders you’re not new to borrowing and you repay the money you owe.

Credit Mix (10%)

There are two different types of credit. Revolving debt includes financial products like credit cards and lines of credit. Installment loans, on the other hand, include auto loans, student loans and mortgages. Lenders want to see that you have experience with different types of credit and use each responsibly.

New Credit (10%)

Applying for any credit account triggers an inquiry on your credit report. Soft inquiries won’t affect your credit score, but a hard inquiry will. Lenders like to see only a few credit inquiries at a time. Many inquiries in a set period could indicate financial trouble.

How To Get A 700 Credit Score

You can hit a 700 score in multiple ways, but you have to work at improving your credit if your credit score is low.

Take the following steps to aim for a credit score of 700 or above.

1. Lower Your Credit Utilization Ratio

Credit utilization makes up the second-largest percentage of your credit score. As a result, using less of your credit limit will likely lead to a higher credit score. You can lower your utilization by paying off loans and credit card balances. You can also ask your credit card issuer to increase your credit limit.

2. Space Out New Credit Applications

Opening multiple new credit accounts will lower the age of your credit history and likely hurt your credit score. You can help prevent a significant dip in your score by only opening one new credit account at a time. Spacing out applications should give your credit score time to recover between inquiries.

3. Diversify Your Credit Mix

A mix of revolving and installment debt shows you can manage various types of credit accounts. For example, if you only have credit cards, you may consider applying for a personal loan. On the other hand, if you only have installment loans, you might consider applying for a credit card or personal line of credit.

4. Keep Old Credit Cards Open

Credit bureaus want to see a long credit history of managing debt with low balances. It may be tempting to close your cards once you consolidate your credit card debt. However, this can harm your score. Instead, leave the accounts open and avoid using your credit cards for big purchases in the future.

5. Make On-Time Payments

Paying off debt and paying on time are even more important than your credit mix and opening new lines of credit. Raising your score won’t work if your history contains late payments or other delinquencies. To make significant improvements to your credit, you’ll need to focus on paying off what you owe in a timely manner.

How Long Does It Take To Get A 700 Credit Score?

The good news is that you can always work to make your credit score higher. The bad news is that it usually takes some time. For example, if you have more than three hard inquiries, you may want to wait before applying for new credit. This limits new inquiries on your credit report. You can also wait up to 24 months for an existing inquiry to potentially “roll off.”

To see faster score improvements, you can pay down balances to lower your debt-to-income ratio (DTI) and credit utilization rate. This will likely yield an improvement within just a few months.

How Many People Have A 700 Credit Score?

Credit scores fall into ranges that lenders use to determine the interest rate to offer you. The ranges are as follows:

- Exceptional: 800+

- Very Good: 740 – 799

- Good: 670 – 739

- Fair: 580 – 669

- Poor: 579 and below

The average credit score in America is 716, according to FICO®. Their research also shows that older generations – Generation X, baby boomers and the Silent Generation – have average credit scores above 700.

While this data may seem to indicate it takes until midlife to achieve “good credit” status, the average millennial has a credit score of 686, meaning they aren’t far away from a 700 credit score. In this position, they can easily achieve a 700 score with good credit habits.

Final Thoughts

A credit score of 700 or above can open a lot of financial doors for you. It can also make you extremely creditworthy in the eyes of lenders. A 700 credit score may qualify you for a lower interest rate and many loan options. Knowing what affects your credit can make it easier to maintain a good or excellent score.

Want to see what personal loan rates your credit score can get you? Get prequalified today with Rocket Loans.

Apply For A Personal Loan.

Getting a personal loan has never been easier.

The Rocket LoansSM application process makes borrowing simple.

Apply NowVictoria Araj

Victoria Araj is a Section Editor for Rocket Mortgage and held roles in mortgage banking, public relations and more in her 15+ years with the company. She holds a bachelor’s degree in journalism with an emphasis in political science from Michigan State University, and a master’s degree in public administration from the University of Michigan.

Related Resources

Viewing 1 - 3 of 3